Companies can either buy or lease assets it needs on a long-term basis. For example, a firm can buy a truck required for the business or lease the truck. A company usually leases a long-term asset if it either 1) does not have the money to buy it and 2) does not want to borrow the capital required to buy these assets. The business case should be the driver of this decision. Sometimes, companies may lease the asset because it does not have money to buy the asset or wants to avoid taking on more debt.

What is a Lease?

A lease is defined as a contractual agreement in which one party allows another party to use an asset for a specific period of time in exchange for defined periodic payments. The asset could be land, building, equipment, websites, brands, or anything else.

Finance Lease vs. Capital Lease vs. Operating Lease

In trying to understand the difference between a finance lease, a capital lease, and an operating lease, first, let’s be clear that all three are leases as defined above. There is no difference whatsoever between the three leases on the ground. The only difference is in the way they are treated in the accounting books. Because they are treated differently in the accounting book, they will impact the financial statements in different ways. We will look at how these different leases impact the books in this article.

Finance Lease vs. Capital Lease

Second, let us also understand that the finance lease and a capital lease mean exactly the same thing. Because the finance lease and capital lease and one and the same, there is no difference in the way they are accounted for. An operating lease is treated differently. How are the finance lease and operating lease different?

Accounting Treatment of Finance Leases (or Capital Leases) vs. Operating Leases

An operating lease is expensed like every other expense in the period it was incurred. On the other hand, a finance lease or a capital lease is capitalized and treated as an asset in the accounting books. We detail out how a finance lease or a capital lease is capitalized and treated as an asset in the accounting books and how it impacts the financial statements later in this article.

Distinguishing Between Finance Leases (or Capital Leases) vs. Operating Leases

As indicated earlier, there is no difference between a finance lease, a capital lease, and an operating lease on the ground. The only difference between these leases is in the way they are treated. The conditions of the lease specified in the lease agreement determine if a lease is classified as a finance lease or an operating lease.

Accounting rules specify the conditions required to treat an operating lease as a capital lease and capitalize it. Treat an operating lease as a capital lease and capitalize the asset simply means we must take an operating expense (lease payment) and treat it as an asset or a capital item.

FASB Prescribed Accounting Rules for Leases in the US

In the US, the Financial Accounting Standards Board’s (FASB) new accounting standard (ASU 2016-02) deals with the rules for reporting operating lease assets and operating lease liabilities in financial statements. If the operating lease meets any of the following conditions, it must be treated as a capital lease and capitalized:

- The lease transfers ownership of the property to the lessee by the end of the lease term;

- The lease contains a bargain purchase option;

- The lease term is equal to 75% or more of the estimated economic life of the leased property. However, if the beginning of the lease term falls within the last 25% of the total estimated economic life of the leased property, including earlier years of use, this criterion shall not be used for purposes of classifying the lease; and

- The present value of the minimum lease payments, excluding that portion of the payments representing executory costs such as insurance, maintenance, and taxes to be paid by the lessor, including any profit thereon, equals or exceeds 90% of the excess of the fair value of the leased property to the lessor.

IFRS Prescribed Accounting Rules for Leases (International Standards)

The IFRS, which prescribes the regulation for international companies, has one additional criterion that involves the asset’s nature!

5. If the leased asset is customized or specialized for the lessee such that only the lessee can use it without significant changes being made, then the operating lease will be treated as a finance or capital lease and capitalized as an asset.

Operating and Finance Lease Disclosures in Form 10-K / Annual Reports

Over the years, companies have gotten away with minimum disclosures on leases. They have been able to hide off-balance-sheet financing via leases. However, accounting regulation now requires companies to specify the following so investors have more clarity on mandatory payment obligations impacting financial health and make informed investing decisions. Today, accounting standards (ASU 2016-02) require companies to disclose:

- All committed annual payments payable in the future in operating leases signed.

- The NPV of the committed annual payments payable in the future in operating leases signed. This is what is reflected in the balance sheet as a leased asset and leased asset liability

- The discount rate assumed to discount the future lease payments to arrive at the net present value of future obligations.

What are the steps involved in converting an operating lease into a capital lease?

We address the steps required to capitalize an operating lease below.

- Value the operating asset: You value the operating asset by summing up the present value of all committed lease payments. Use the pre-tax cost of debt as the discount rate assuming you borrowed money at that rate to fund the asset.

- Leased Asset Liability in the Balance Sheet: The value of the operating asset arrived at above is considered as debt. This is reflected in the liabilities side of the balance sheet as a line item as a Leased Asset Liability.

- Leased Assets in the Balance Sheet: The value of the operating asset arrived at above is considered the gross value of the operating asset. The gross value of the operating asset is reflected in the assets side of the balance sheet in a line item – Gross Value of Leased Assets.

- Depreciation of Leased Asset in the Income Statement: The leased asset is depreciated at the appropriate depreciation rate. The depreciation each year is expensed in the income statement.

- Net Book Value in the Balance Sheet: The leased asset is depreciated at the appropriate depreciation rate and captured in the accumulated depreciation of the leased asset. The Net Book value of the leased asset is the gross book value less the accumulated depreciation of the leased asset and is placed in the balance sheet under property, plant, and equipment or assets.

- Operating Lease vs Interest Expense & Depreciation in the Income Statement: The operating lease expense is removed in the income statement. In place of the operating lease, you will have interest expenses on the leased asset liability and depreciation of the leased asset.

What impact does capitalizing an operating lease have on a company’s financial statements?

As seen above, capitalizing an operating asset involves adjustments to the income statement and balance sheet. We address this question with a full model in detail in our private equity and investment banking question list here.

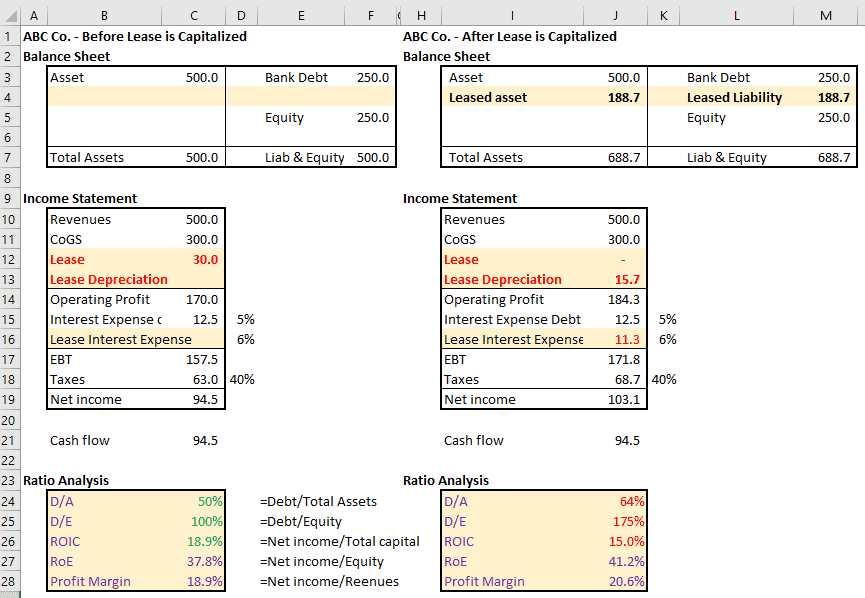

Example of capitalizing an operating lease on a company’s financial statements

We have shown below the impact of capitalizing an operating lease on a company’s financial statements. Note that the financial statements on the left side are statements before any adjustment is done. The financial statements on the right side are the financial statements after the operating lease capitalization adjustments are done.

Pay special attention to the financial ratios to understand how capitalizing an operating lease on a company’s financial state impacted the company’s financial statements.

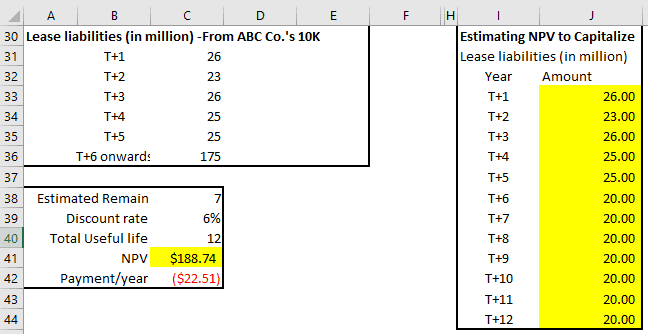

How do you estimate the value of the Leased Asset?

The value of the leased asset is assumed to be the NPV of all lease payments committed in the lease agreement. The value of the leased asset is estimated from the lease disclosures in the company’s 10K statement. Given below is an example with the excel model.

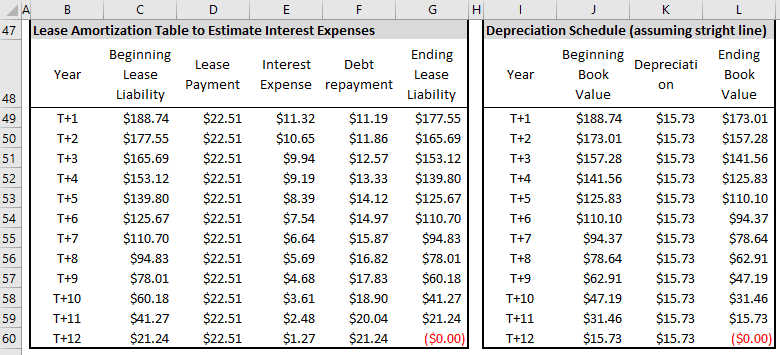

Leased Liability and Leased Liability Interest Expense

Accounting regulation also requires a liability to be added for the leased asset. Often called a Leased Asset Liability, a new liability equal to the value of the leased asset computed above is also added to the balance sheet on the liabilities side. Computation of the Leased Liability Interest Expense is shown below.

Depreciation on Leased Asset

Because we have to show the leased asset on our balance sheet, we assume the use of these assets will incur a corresponding depreciation expense. We have assumed a simple straight-line depreciation on the asset in the example above. In practice, a MACRS schedule for the corresponding asset life or another appropriate depreciation method can be used to estimate the depreciation expense in the income statement.

Accumulated depreciation is set off against the gross asset value to get the net book value of the leased asset in the balance sheet.